The basis for concern

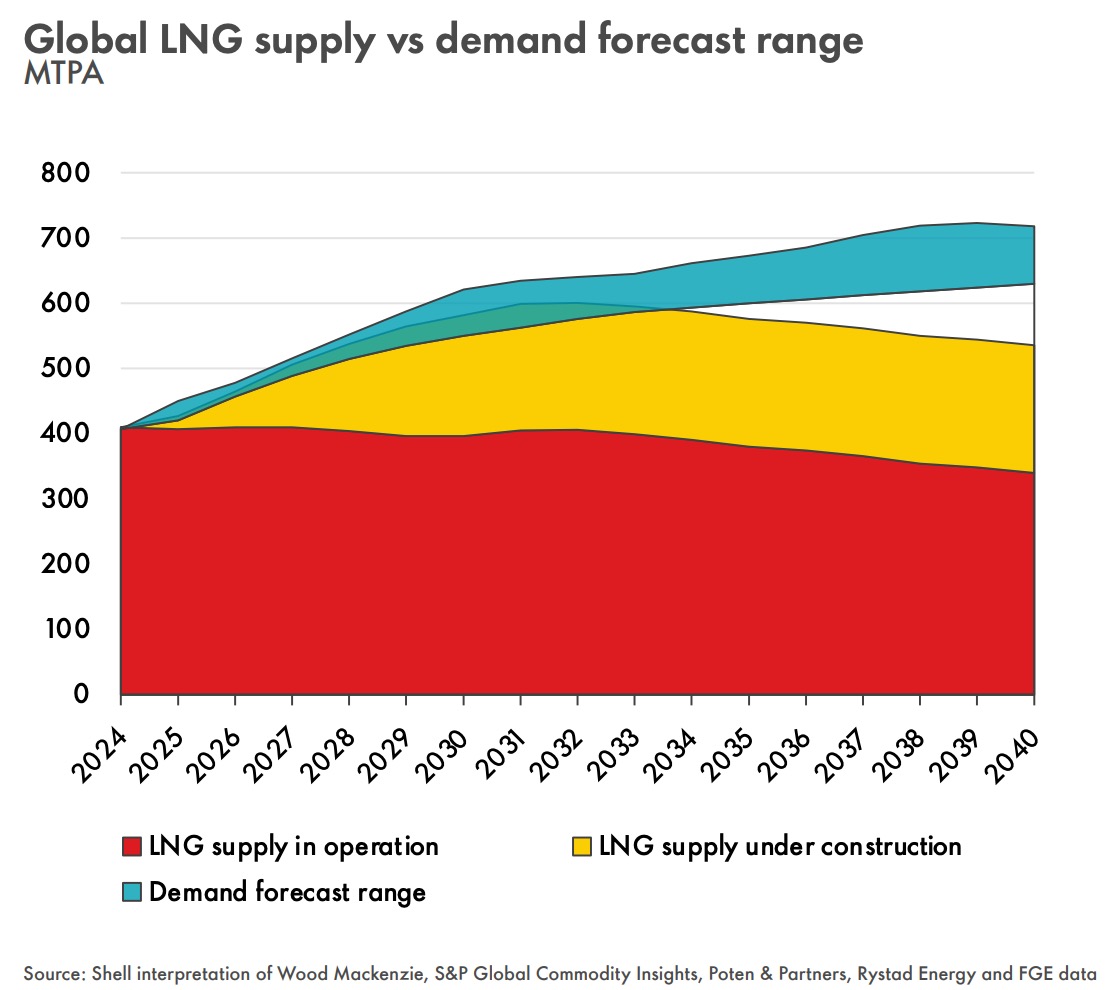

Based on a stellar reputation for in-depth scenario planning, Shell’s energy market assessments have for over 50 years been consulted by other companies for investment and portfolio planning. Shell’s latest, the LNG Outlook 2025, indicates (ref. caption slide) that the LNG market will be in balance until year 2031 and then need an additional 133 mtpa LNG supply to year 2040 to cover demand increase to 670 mtpa and depleting feedgas volumes to older LNG plants.

Remarkably, having scaled up significantly in recent years, equipment suppliers and EPC contractors appear technically able to accommodate all projects now lined up for FID for startup in the 2029-2040 timeframe.

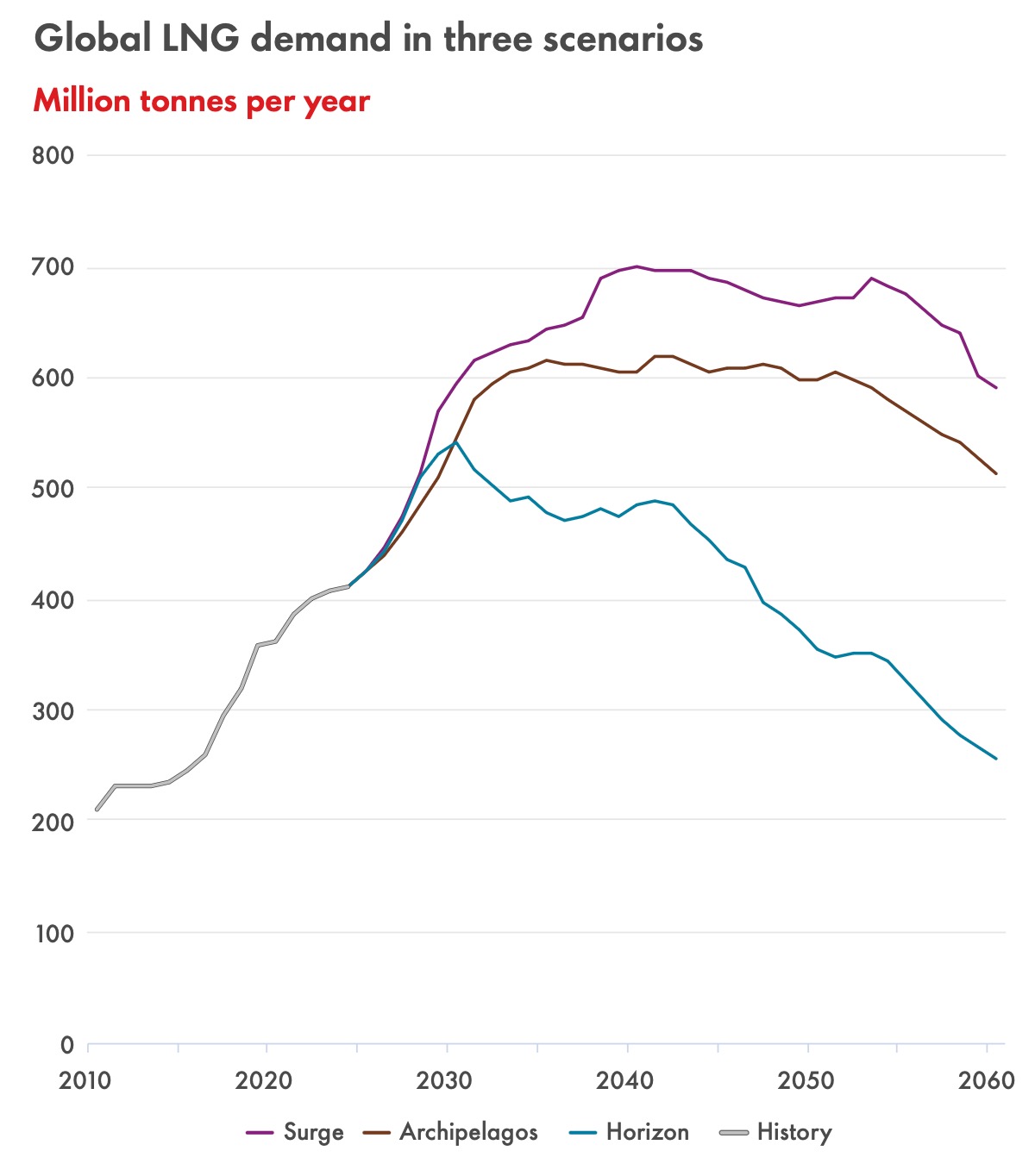

This year, however, Eikland Energy is concerned that the brief and elegant LNG Outlook may be misleading in failing to include or mention essential information and richer perspectivers from the comprehensively developed three demand scenarios in Shell’s separately released 2025 Energy Security Scenarios report.

Shell’s LNG Outlook 2025 appears to borrow strongly from the high growth ‘Surge’ scenario but, untypically, there are multiple references to ‘Shell interpretation’ of assessments by several consulting firms. These references suggest that the LNG Outlook has been crafted by a different Shell team. In Eikland Energy’s experience several of the named firms have historically had demand forecasts on the high end, which could point to greater risk if the post-WW2 free trade paradigm is threatened.

While there are indirect references in the LNG Outlook 2025 to the now arguably more relevant ‘Archipelago’ scenario from the Energy Securities Scenarios report – that has LNG demand flattening at 600 mtpa from 2032 – this is not carried into the demand outlook. The ‘Archipelago’ scenario describes a world drifting into isolationist blocks where free trade is impeded, anticipating a generalization of mercantilism. Perspectives from the CO2-focused ‘Horizon’ scenario, which has global LNG demand peaking at about 500 mtpa to 2040 and then falling, are totally missing.

It is incidentally remarkable that none of the reports mention uncertainties regarding lifting of LNG sanctions on Russia and resumption of natural gas exports to Europe. The assessed 2030 European LNG demand of the LNG Outlook shows no resumption of sanctioned and curtailed Russian gas to Europe, however. This corresponds to ca. 40 mtpa equivalent of potentially reduced new LNG demand, via pipeline gas substitution and LNG directly. Recent Ukraine truce talks appear to have at least a partial lifting of sanctions on the table.

A more prudent approach

Eikland Energy believes that there was market evidence even as early as spring 2021 to support a change from Shell’s ‘Surge’ scenario as base case, to the ‘Archipelago’ scenario. Some of the drivers were the Suez Canal blockage by Ever Given, Panama Canal draught and capacity constraints, and Houthi ship attacks near the Bab al-Mandab Strait. The transition to ‘Archipelago’ as new base case appears to have been finally set with the commencement of the second Trump presidency.

Prevailing uncertainties and threats to global trade are likely to have both near-term effects and longer term structural consequences for demand overall and globalized LNG trade well beyond 2028. Increased geopolitical risk, a loss of trust and stability is already being strongly reflected in business decisions world-wide.

Worryingly, these factors are all strong accelerators for demand contraction, with no identified upside potential that has not already been accounted for. Eikland Energy therefore recommend:

- Positing that the 600 mtpa LNG demand level of the ‘Archipelago’ scenario is now the most plausible 50/50 reference case towards 2040.

- Accepting that the widely accepted near-linear growth in LNG demand to 2032, and the associated supply-demand balance, may be at risk.

- Seeing it likely that Russian gas may return to Europe at the 20 mtpa equivalent level by year 2030, but not grow materially beyond this before 2040.

These assessments and recommendations are likely to lead to major and structural changes in portfolios and business decisions generally in the years ahead. In particular, it should not be assumed that the market is likely to be generally balanced in the period to 2031. The implications for business strategy are:

- To focus on developing strong near-term and long-term optionalities.

- To use upcoming FIDs as fast follow-up for portfolio rebalancing

- Build and preserve flexibility for dynamic change of priorities.

- Limit opportunistic investments and engagements to the medium-term.

For LNG shipping specifically the recommendations imply that the existing fleet and order book already covers a substantial part of firm tonne-mile requirements into the 2030-2040 period. Any new ship order should therefore be backed by a long-term charter.

LNG project competition

Eikland Energy has revisited and ranked all matured pre-FID LNG supply projects worldwide. Of the 375 mtpa total undecided capacity, 150 mtpa target FID in 2025 or early 2026. However, only about 15 ‘world scale’ trains of 5 mtpa each are required if the global new LNG capacity requirements to 2040 falls to around 75 mtpa with the ‘Archipelago’ base case.

Even this is optimistic when accounting for a possible return of some Russian gas to Europe and the likely extra capacity from de-bottlenecking of plants now under construction.

In 2023 and 2024 US LNG plants at large formalized a better than 5% capacity upgrade by having their DOE export permit limits lifted. There is also long historical precedent for this and Eikland Energy conservatively assumes an average 5% capacity addition, or 15-20 mtpa, from stramlining and de-bottlenecking new projects withing 5 years of startup.

Plant debottlenecking and a limited return of Russian gas to Europe could therefore potentially to reduce incremental, ‘market-balanced’, 2040 LNG supply requirements to 50 mtpa.

Since the average new LNG liquefaction project will have a design capacity of 10-20 mtpa there will nominally only be room for 4-6 new such projects in the 2040 time frame. This will also include Phase II expansion decisions on projects such as LNG Canada, Coral and Tortue.

LNG project ranking and selection

Eikland Energy considers that both US and non-US LNG projects can each easily fully provide necessary new LNG supplies required for 2040 under the ‘Archipelago’ scenario that Eikland Energy consider as a base case.

Until about 2022, US projects benefitted from low feed gas prices, assured dry gas supply from the shale-gas revolution, a flexible gas pipeline system, brown-field advantages and associated very short project development time. International projects usually required a full development from the field, including liquids handling.

Short development time is now less critical for new projects with the current pipeline of projects under construction and insecurity about future demand. In addition, there is growing concern that a strengthening of Henry Hub prices (and occational feed gas interruptions from US demand peaks) will no longer assure supply security and a previously comfortable trading margin.

Instead, international projects now appear to be favored to balance a combination of portfolio factors. This includes logistics, price index exposure and expected price, as well as new political risk. In Asia in particular, Qatar and UAE have both been very successful at rapidly securing buyers for new vertically integrated projects. As part of this trend, Eikland Energy sees stronger focus on replacing declining LNG exports from Indonesia and Malaysia, close to 35 mtpa between 2025 and 2040, with nearby regional sources, including now also East African projects.

Buyers are therefore in a strong position to steer the firm part of their future supply portfolio balance, and timing for commitment. Eikland Energy’s assessment is that both traditional buyers and oil companies now lean strongly to non-US projects for long-term firm supplies, but may also set explicit supply portfolio diversification targets.

Based on a project-by-project assessment, 85% of new near FID-ready US LNG on offer seems likely not be realized unless developed substantially based on a merchant platform. The current dynamically traded, ‘liquid’, global LNG market could indeed justify FID for a well-backed project willing to assume commodity and price risk. There is already evidence that at least four US project developers and gas producers are leaning in this direction. If they proceed, it could possibly preempt development of mainly other US projects.

Even if they are strongly prioritized by portfolio rebalancing, international LNG projects will also be challenged. Eikland Energy expect that fewer than 50% of international FID-ready projects will be realized within the 2040 time frame.

— * * * —

The assessments discussed in this note may of course not be shared by the investment community and company boards ultimately facing the final investment decision. The scale and pervasiveness of the uncertainties introduced by the increased trade barriers of mercantilism nevertheless suggest that several planned FIDs for projects Eikland Energy has examined will be delayed, but also that some projects will be accelerated.

US tariffs have the effect of immediately penalizing US LNG export projects, old and new. Apart from deterring international buyers’ trust in the security of supply under existing contracts, aluminum and steel prices, gas compressors, and US natural gas prices all rise to penalize US LNG export projects.

Eikland Energy expect DOE deadlines for final investment decisions in new LNG projects to be revisited and extended. Postscript: After this note was originally published on April 2, on April 3 the US DOE released the “10 CFR Part 590: Rescission of Policy Statement on Export Commencement Deadlines in Authorizations To Export Natural Gas to Non-Free Trade Agreement Countries”. This new order will effectively give automatic extension of project startup deadlines on good cause. Eikland Energy believes the increased leniency implied by the new policy in part is a reflection of feedback from projects under development and that changing market sentiments are already taking hold.

Conversely, the are already signs that responses to increased US tariffs will in 2025 include statements of intent, importantly also at the national level, to reduce exposure to the US and the accelerate selected quality non-US projects, such as developent of LNG Canada phase 2 and the Coral Norte FLNG. In the near term maybe even by e.g. China taking the challenge to accept LNG from the sanctioned ALNG2.

A number of options are on the table, and the Archipelago scenario is taking hold.