US shale oil could drop by 0.5 mill. Bbls/day in 2015

At current oil prices, there is momentum for stabilization and then contraction of US shale oil production through 2015 and beyond. The full output reduction…

At current oil prices, there is momentum for stabilization and then contraction of US shale oil production through 2015 and beyond. The full output reduction…

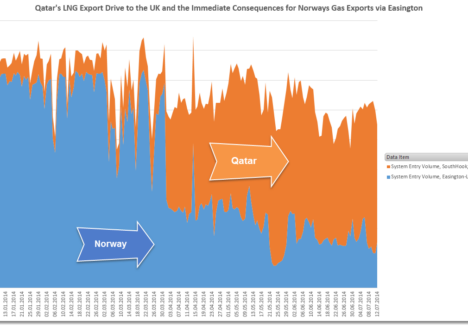

After several years of struggle, natural gas is again “in merit” in marginal price terms in broad parts of Europe and in the rest of…

This 23 December 2014 post (republished 23.January 2015 due to system restore) is a follow-up of our November comments on OPEC thinking and market strategy…

The LNG World Summit 2014 takes place in Paris this week and we look forward to attending this important event. Risk management is a key…

In year 2005 investment bank Goldman Sachs famously asked “What does it take to stop China?” They answered the question themselves, an oil price of…

As recent tumultuous energy market events have shown, the value of, and need for powerful business intelligence has never been greater. Market information and tools…

Overstocked gas storage facilities and a mild winter have been blamed for the strong fall in European spot gas prices in 2014. However, the surprising…

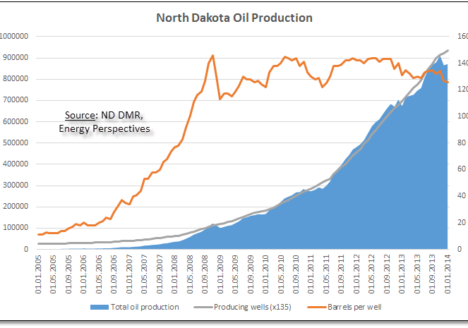

The explosive growth in North Dakota oil production, mainly driven by exploration in the Bakken and underlying Three Forks shales structures, has driven a resurgence…

The complex Ukrainian and Crimean situation has an abundance of Cold War, WW2, and maybe even Ottoman Empire parallels, leading back to the early days…

Yet that was the situation on some key locations on 5 February 2014, and typical prices were well above the magical crude oil parity of…

The images of burning water and the resulting environmental discussions in the past two years have faded and natural gas production from the Marcellus shale is…

Energy Perspectives is pleased to release a whitepaper on coming US LNG exports. The US gas price fall in 2011 and international demand growth has…

Gulf of Mexico oil and gas production activities have now generally been restored to the level before the 2010 Macondo blowout. Drilling bans have been formally…

The communique from the third Chinese communist party plenum on the 12th of November states that “markets will play a decisive role in the allocation…

The announcement of a Heads of Agreement between CNPC and Novatek for a minimum annual delivery of 3mt of LNG to China is highly significant,…